TODAY IS

Latest topics

Sun 29 Aug 2021, 22:15 by Jude

Sun 29 Aug 2021, 22:15 by JudeTHE OLIVE BRANCH | GOD IS MY SALVATION

LIVE TRAFFIC FEED

ZERO HEDGE - JPM: "TURNING POINTS IN MARKET TRENDS ARE OCCURRING AT THE FASTEST PACE IN HISTORY"

END TIME NEWS, A CALL FOR REPENTANCE, YESHUA THE ONLY WAY TO HEAVEN :: CHRISTIANS FOR YESHUA (JESUS) :: ZERO HEDGE

Page 1 of 1

ZERO HEDGE - JPM: "TURNING POINTS IN MARKET TRENDS ARE OCCURRING AT THE FASTEST PACE IN HISTORY"

![]() Jude Sat 04 Feb 2017, 17:55

Jude Sat 04 Feb 2017, 17:55

JPM: "Turning Points In Market Trends Are Occurring At The Fastest Pace In History"

by Tyler Durden

Feb 4, 2017 11:26 AM

Ever get the feeling that the market has become frustratingly fast in responding to new information, with violent swings in either direction coming ever faster even if ultimately the "BTFD" mentality always seems to prevail? Well, it's a fact.

As JPM reports in a new analysis, citing quantitative and qualitative metrics, markets have become more macro driven and react faster to the new information. A qualitative example below shows the reaction time for recent major events (August ’15 selloff, Brexit, US Election, Italy Referendum) that has compressed from weeks to hours (Figure below).

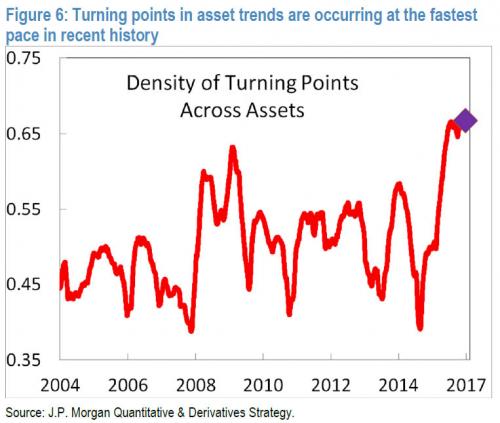

In empirial terms, this means that quantitatively, we are noticing a higher density of market turning points. The next figure shows the average variability of asset trends (averaged across major asset classes) that show turning points occurring at the fastest pace in recent history (~30 years).

Given the engagement of central banks with markets and geopolitical developments, it should not be a surprise that markets are more macro driven. Furthermore, thanks to the ubiqutous presence of collocated HFTs, which respond to to headlines in microseconds, not to mention that information is created and consumed at a much faster pace than e.g. a decade ago (think of twitter, smartphones, etc.), the market is generally much "faster."

As JPM's Marko Kolanovic also points out, "an emerging class of fully automated quant strategies is also likely speeding up the market reaction – these strategies process and trade on new information (e.g. feeds from tweets, press releases, etc.) in real time. Finally, we now live in a world in which everyone is a momentum chasers. As a result, the increased popularity of trend following strategies is also likely to contribute to shorter and faster trends, as strategies react quicker and lead to potential over/undershooting of fundamentally justified levels."

What are the implications of this fast-moving market? Some further thoughts from JPM:

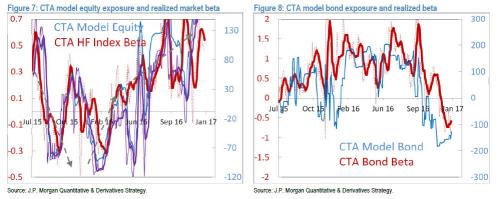

Macro investors cannot ignore these developments, as they will need to react faster, compete with machines, and will be left with more risk in the form of market turning points. CTAs provide a good illustration of the direct of impact of quant strategies on asset flows. Figure 7 shows estimated equity flows, and Figure 8 estimated bond flows (the red line is actual exposure of a broad CTA index to the asset class, i.e. fund beta, and blue line is our model based out-of-sample forecast of the same position – note close correlation between the two). In 2015 and early 2016 these investors took substantial positions in equities, and the recent shift from a record long to short bond position contributed to a widening of bond yields.

Fundamental stock investors cannot ignore quant strategies either. Stocks are increasingly driven by (market neutral) factor exposures at the expense of fundamental drivers. Figure 9 illustrates this for one particular low volatility stock (JNJ, correlation to sector vs. correlation to low vol factor). Ten years ago, JNJ stock returns were entirely driven by sector fundamentals, but currently half of the stock’s returns are driven by factor returns (low vol factor). We also notice an outsized impact of stock returns around quant rebalances that typically occur at the end of the month (and first week of the month). Figure 10 shows that probability of a large move for stocks in a momentum portfolio are up to 3 times as large during turn of the month rebalances, as compared to other days in a month.

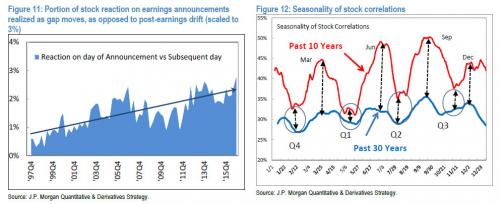

That said, fast moving markets are becoming a problem for everyone, not just macro investors. Stocks are reacting quickly to news, which leaves human investors less time to act. An example is earnings announcements where stocks immediately adjust to a price level and there is very little post-earnings drift. Figure 11 shows the size of earnings moves (normalized to ~3%) that are realized as gap moves (as opposed to post earnings drift) over time. Note that over the past decade, earnings drift has largely disappeared as stock prices adjust instantaneously. Similarly, market correlation started exhibiting strong seasonality – they are high outside of earnings season, and quickly break down at the time of announcement. This seasonality is further exacerbated by the increase of passive assets that drive correlation higher (outside of earnings season).

Furthermore, the ongoing mega-shift of funds from active to passive strategies continues to distort the "efficient market."

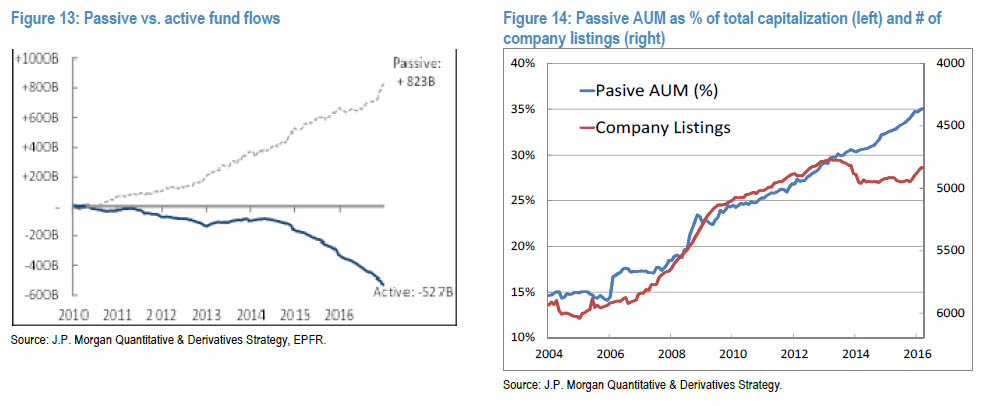

According to JPM, the level of passive indexation reached all-time highs with estimated ~35% of equities invested in capitalization weighted indices (up from ~15% 10 years ago). If indexed assets are relatively small, passive investing is a great cost-effective strategy. Passive investors are effectively piggy-backing on the most efficient, optimal, market portfolio. However, if the asset base becomes too large, passive investing may prevent market efficiency and lead to a misallocation of capital (large companies get larger, and small ones do not have capital, regardless of fundamentals). A large increase in passive assets can also cause distortion of valuations (e.g. favoring momentum vs. value, large vs. small, etc.). Investors are increasingly asking whether the current level of passive assets is already a problem for markets, and even the economy as a whole.

Figure 13 shows the recent trend in passive vs. active flows, and Figure 14 shows the increase in passive equity assets (as a % of total equity assets) as well as the number of companies listed in the US (on an inverse scale). There is a significant negative correlation between the number of new listings and size of passive assets. Although the correlation between the two is highly significant, this does not necessarily mean that passive assets caused this decline of new listings. The trend of capitalization weighted indexation may peak and start reverting over the next few years, especially if factor and stock dispersion cause broad capitalization weighted indices to underperform.

What is the preliminary conclusion? Well, for human investors competing with algos, robots and "Artificial Intelligence", will become even more difficult, not least of all because so much capital has shifted and continues to flow from active to passive strategies. As a result, ordinary, carbon-based investors will find they are increasingly at a disadvantage, even as the market drift from "fair value" continues to grow, making a major market "repricing" event increasingly more likely, while assuring that the losses for active market participants, mostly of the electonic variety will be dire.

Unfortunately, with few regulators able to grasp the major shift below the market's surface, and especially now that deregulation is about to sweep Wall Street, there is little hope any of these concerns will be addressed until it is too late. In the meantime, prepare for markets that keep getting even faster, even more micro-volatility, even if the BTFD impulse continues to prevail until one day, the disconnect is just to great and the long overdue "mean reversion" event finally kicks in.

FOR MORE ON THIS ARTICLE, PLEASE VISIT: http://www.zerohedge.com/news/2017-02-04/jpm-turning-points-market-trends-are-occurring-fastest-pace-history

by Tyler Durden

Feb 4, 2017 11:26 AM

Ever get the feeling that the market has become frustratingly fast in responding to new information, with violent swings in either direction coming ever faster even if ultimately the "BTFD" mentality always seems to prevail? Well, it's a fact.

As JPM reports in a new analysis, citing quantitative and qualitative metrics, markets have become more macro driven and react faster to the new information. A qualitative example below shows the reaction time for recent major events (August ’15 selloff, Brexit, US Election, Italy Referendum) that has compressed from weeks to hours (Figure below).

In empirial terms, this means that quantitatively, we are noticing a higher density of market turning points. The next figure shows the average variability of asset trends (averaged across major asset classes) that show turning points occurring at the fastest pace in recent history (~30 years).

Given the engagement of central banks with markets and geopolitical developments, it should not be a surprise that markets are more macro driven. Furthermore, thanks to the ubiqutous presence of collocated HFTs, which respond to to headlines in microseconds, not to mention that information is created and consumed at a much faster pace than e.g. a decade ago (think of twitter, smartphones, etc.), the market is generally much "faster."

As JPM's Marko Kolanovic also points out, "an emerging class of fully automated quant strategies is also likely speeding up the market reaction – these strategies process and trade on new information (e.g. feeds from tweets, press releases, etc.) in real time. Finally, we now live in a world in which everyone is a momentum chasers. As a result, the increased popularity of trend following strategies is also likely to contribute to shorter and faster trends, as strategies react quicker and lead to potential over/undershooting of fundamentally justified levels."

What are the implications of this fast-moving market? Some further thoughts from JPM:

Macro investors cannot ignore these developments, as they will need to react faster, compete with machines, and will be left with more risk in the form of market turning points. CTAs provide a good illustration of the direct of impact of quant strategies on asset flows. Figure 7 shows estimated equity flows, and Figure 8 estimated bond flows (the red line is actual exposure of a broad CTA index to the asset class, i.e. fund beta, and blue line is our model based out-of-sample forecast of the same position – note close correlation between the two). In 2015 and early 2016 these investors took substantial positions in equities, and the recent shift from a record long to short bond position contributed to a widening of bond yields.

Fundamental stock investors cannot ignore quant strategies either. Stocks are increasingly driven by (market neutral) factor exposures at the expense of fundamental drivers. Figure 9 illustrates this for one particular low volatility stock (JNJ, correlation to sector vs. correlation to low vol factor). Ten years ago, JNJ stock returns were entirely driven by sector fundamentals, but currently half of the stock’s returns are driven by factor returns (low vol factor). We also notice an outsized impact of stock returns around quant rebalances that typically occur at the end of the month (and first week of the month). Figure 10 shows that probability of a large move for stocks in a momentum portfolio are up to 3 times as large during turn of the month rebalances, as compared to other days in a month.

That said, fast moving markets are becoming a problem for everyone, not just macro investors. Stocks are reacting quickly to news, which leaves human investors less time to act. An example is earnings announcements where stocks immediately adjust to a price level and there is very little post-earnings drift. Figure 11 shows the size of earnings moves (normalized to ~3%) that are realized as gap moves (as opposed to post earnings drift) over time. Note that over the past decade, earnings drift has largely disappeared as stock prices adjust instantaneously. Similarly, market correlation started exhibiting strong seasonality – they are high outside of earnings season, and quickly break down at the time of announcement. This seasonality is further exacerbated by the increase of passive assets that drive correlation higher (outside of earnings season).

Furthermore, the ongoing mega-shift of funds from active to passive strategies continues to distort the "efficient market."

According to JPM, the level of passive indexation reached all-time highs with estimated ~35% of equities invested in capitalization weighted indices (up from ~15% 10 years ago). If indexed assets are relatively small, passive investing is a great cost-effective strategy. Passive investors are effectively piggy-backing on the most efficient, optimal, market portfolio. However, if the asset base becomes too large, passive investing may prevent market efficiency and lead to a misallocation of capital (large companies get larger, and small ones do not have capital, regardless of fundamentals). A large increase in passive assets can also cause distortion of valuations (e.g. favoring momentum vs. value, large vs. small, etc.). Investors are increasingly asking whether the current level of passive assets is already a problem for markets, and even the economy as a whole.

Figure 13 shows the recent trend in passive vs. active flows, and Figure 14 shows the increase in passive equity assets (as a % of total equity assets) as well as the number of companies listed in the US (on an inverse scale). There is a significant negative correlation between the number of new listings and size of passive assets. Although the correlation between the two is highly significant, this does not necessarily mean that passive assets caused this decline of new listings. The trend of capitalization weighted indexation may peak and start reverting over the next few years, especially if factor and stock dispersion cause broad capitalization weighted indices to underperform.

What is the preliminary conclusion? Well, for human investors competing with algos, robots and "Artificial Intelligence", will become even more difficult, not least of all because so much capital has shifted and continues to flow from active to passive strategies. As a result, ordinary, carbon-based investors will find they are increasingly at a disadvantage, even as the market drift from "fair value" continues to grow, making a major market "repricing" event increasingly more likely, while assuring that the losses for active market participants, mostly of the electonic variety will be dire.

Unfortunately, with few regulators able to grasp the major shift below the market's surface, and especially now that deregulation is about to sweep Wall Street, there is little hope any of these concerns will be addressed until it is too late. In the meantime, prepare for markets that keep getting even faster, even more micro-volatility, even if the BTFD impulse continues to prevail until one day, the disconnect is just to great and the long overdue "mean reversion" event finally kicks in.

FOR MORE ON THIS ARTICLE, PLEASE VISIT: http://www.zerohedge.com/news/2017-02-04/jpm-turning-points-market-trends-are-occurring-fastest-pace-history

Jude- Admin

- Join date : 2010-12-13

Location : United States -

» ZERO HEDGE - RBC EXPLAINS WHY THE MARKET IS DUMPING, ADDS "THIS IS NOT THE BIG SHORT" ... YET

» THE ECONOMIC COLLAPSE - GLOBAL RECESSION? THE CANADIAN ECONOMY SHRINKS AT THE FASTEST PACE SINCE THE LAST FINANCIAL CRISIS

» JUDGMENT ON AMERICA? WE ARE ON PACE FOR THE WORST YEAR FOR WILDFIRES IN ALL OF U.S. HISTORY!

» WE HAVE ALREADY WITNESSED THE FIRST 1300 POINTS OF THE STOCK MARKET CRASH OF 2015

» STOCK MARKET CRASH 2015: THE DOW HAS ALREADY PLUMMETED 2200 POINTS FROM THE PEAK

» THE ECONOMIC COLLAPSE - GLOBAL RECESSION? THE CANADIAN ECONOMY SHRINKS AT THE FASTEST PACE SINCE THE LAST FINANCIAL CRISIS

» JUDGMENT ON AMERICA? WE ARE ON PACE FOR THE WORST YEAR FOR WILDFIRES IN ALL OF U.S. HISTORY!

» WE HAVE ALREADY WITNESSED THE FIRST 1300 POINTS OF THE STOCK MARKET CRASH OF 2015

» STOCK MARKET CRASH 2015: THE DOW HAS ALREADY PLUMMETED 2200 POINTS FROM THE PEAK

END TIME NEWS, A CALL FOR REPENTANCE, YESHUA THE ONLY WAY TO HEAVEN :: CHRISTIANS FOR YESHUA (JESUS) :: ZERO HEDGE

Page 1 of 1

Permissions in this forum:

You cannot reply to topics in this forum